Quantitative Easing, Financial Repression, and Why the Middle Class Feels Like the Game Keeps Changing

Most people are working harder than ever, but somehow their money still feels lighter. You can earn more today than you did five years ago and still feel broke or in Africa broeeek. That is not just bad budgeting, and that is not just you being irresponsible with your check. Something deeper is moving inside the financial system, and most folks were never given the language to see it clearly.

Two terms economists and serious investors use to describe part of this reality are quantitative easing and financial repression. Before you click away thinking this is about to be a boring college lecture, let me break it down so a Wall Street analyst and somebody standing on the block can both follow.

What Is Quantitative Easing

Quantitative easing, usually called QE, is when central banks create money digitally and inject it into the financial system to stimulate the economy. In plain language, the government and central banks are trying to keep the machine moving. During crises or slowdowns, they buy government bonds, increase liquidity, lower borrowing costs, and push people to spend and invest. The goal is usually to prevent economic collapse.

But there is a side effect, and the side effect is what hits regular people the hardest. When too much money floods the system without enough real productivity behind it, prices rise. Groceries cost more. Homes cost more. Vehicles cost more. Insurance costs more. Tuition costs more. So while your bank account number might stay the same, your purchasing power quietly shrinks in the background while you sleep.

Street Translation

Imagine everybody on the block suddenly gets handed extra money, but the same number of apartments, cars, and chicken wings still exist. Now everybody is bidding higher for the same stuff. Prices jump. Landlords get bold. The corner store get bold. The car lot gets real bold.

That is one reason inflation can explode after heavy money printing. They printed all that money, then acted surprised when the wings went from six dollars to twelve. They were not surprised. They knew. They just hoped you would not notice.

What Is Financial Repression

This is where it gets serious. Financial repression happens when inflation grows faster than the returns people are earning on their savings. Say your savings account is paying three percent. Inflation is running at six percent. That means your money is actually losing purchasing power every year, even though the number on the screen technically went up. You feel like you are saving. The math says you are bleeding.

This silently hurts savers, retirees, middle class workers, and folks living paycheck to paycheck. Meanwhile, the people who own things tend to come out the other side stronger. Stocks, businesses, real estate, infrastructure, and commodities often rise alongside inflation. The asset holders ride the wave. The wage earners get washed by it.

Street Translation

They got you saving in an account that pay you three percent a year. Then in that same year, everything you actually buy went up six, eight, ten percent. So you were never really saving. You were donating. You were paying a slow tax to people who already own the assets you were too uninformed or too distracted to go buy.

Nobody told you that, did they. They told you to be responsible. Be responsible doing what. Sitting on cash while the value of the cash get burned up like a candle in a hot room. That is the part the financial advice on daytime TV will not say out loud.

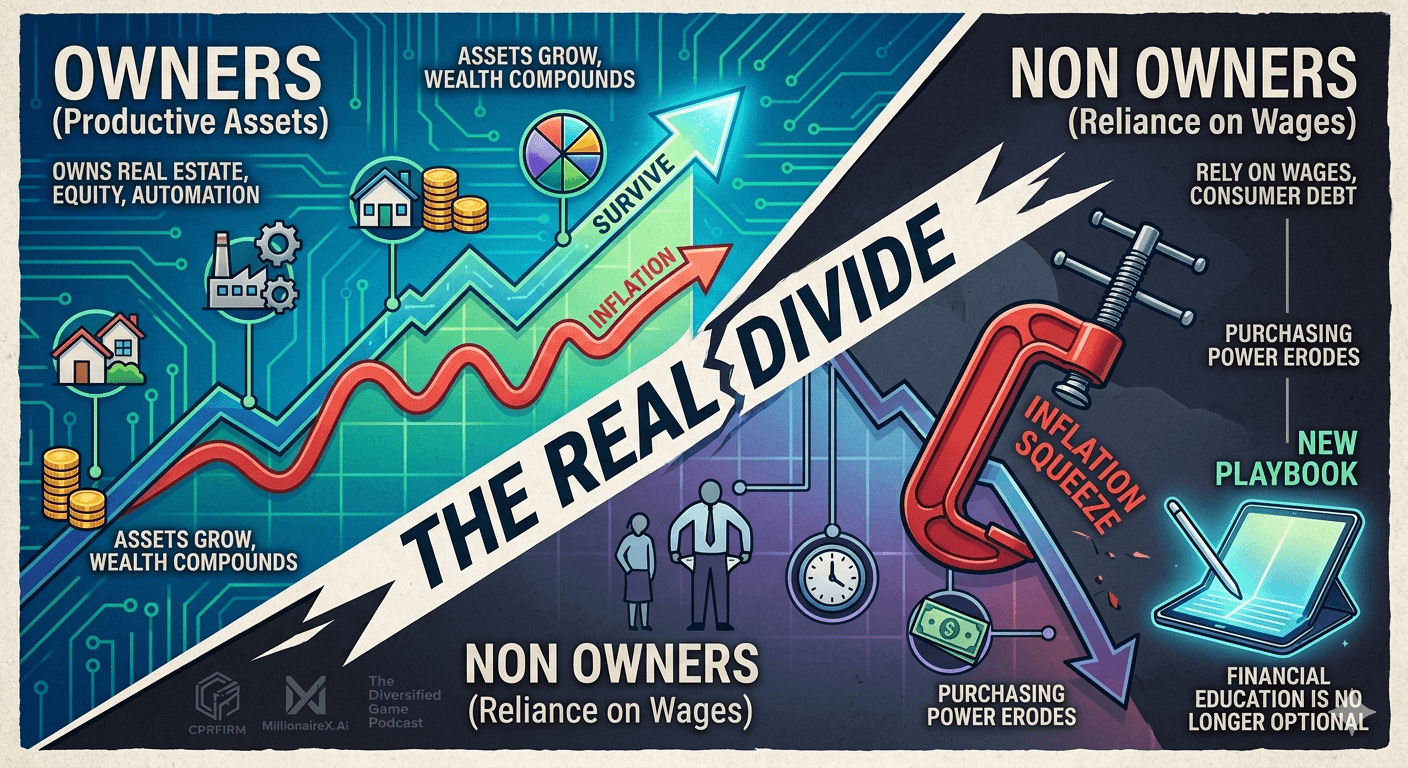

The Real Divide Is Ownership

Here is the part most people miss. The biggest divide in America right now is not just left versus right or red state versus blue state. The biggest economic divide is owners versus non owners.

People who own productive assets tend to survive inflation. People who rely only on wages tend to get squeezed. That is why financial education is no longer optional. That is why I keep telling people through CPRFIRM, through MillionaireX.AI, and through the Diversified Game Podcast that the rules have shifted and you need to learn the new playbook before they finish writing it.

Why Real Estate Investors Often Come Out On Top

A person with a fixed rate mortgage on a property that cash flows can actually benefit during inflationary periods. Rents tend to rise. Property values tend to rise. But that mortgage payment stays right where it was the day they signed the paperwork. Inflation slowly eats away at the real burden of the debt. The bank gets paid back in dollars that are worth less than the dollars they originally lent out.

That is one reason wealthy families love hard assets and pass them down for generations. If you ever wondered why old money never panics about inflation the way regular folks do, that is your answer. They positioned themselves on the side of the equation that wins when the dollar weakens.

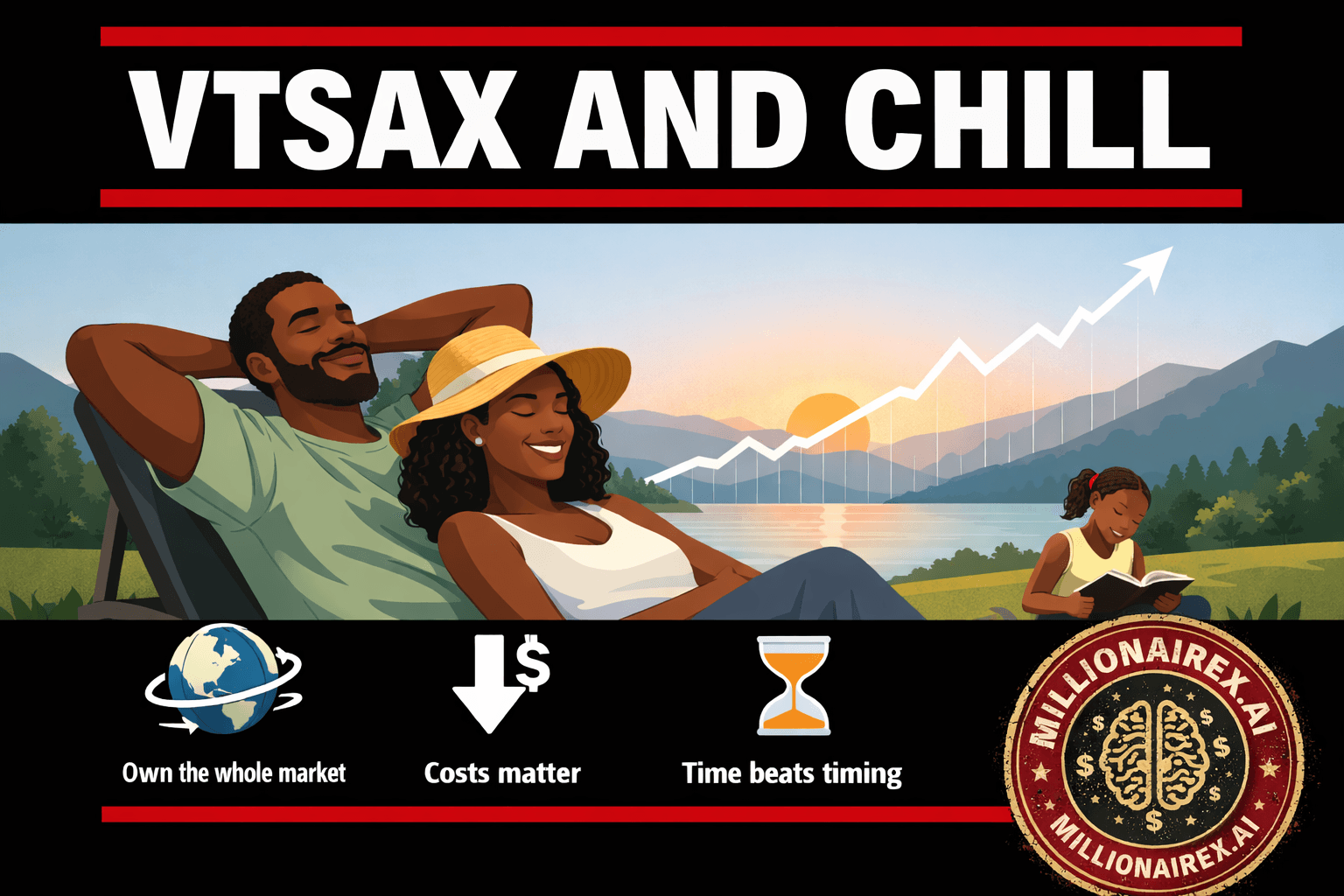

What About Mutual Funds and Retirement Accounts

Broad market index funds like VTSAX or total market funds still represent ownership in real businesses. Businesses adapt. Strong companies raise their prices, automate their operations, expand globally, and innovate faster than their competition. That is one reason many long term investors still believe in diversified market ownership despite the volatility along the way.

But concentration risk is real. A lot of the major funds today are heavily weighted toward a handful of giant technology companies. If those sectors slow down, retirement accounts can feel the pressure quickly. Diversification on paper is not the same thing as diversification in reality. Look under the hood of your fund and see what you actually own.

So Who Gets Hurt the Most

Usually the people holding only cash, retirees depending on fixed income, overleveraged consumers, people without assets, and people waiting for somebody else to come save them. The system is not personal. It does not hate you. It just rewards positioning, and positioning requires knowledge most people were never given.

Street Translation

You are out here mad at the gas pump. Mad at the grocery store. Mad at the rent letter. But being mad will not buy you a single share of nothing. Being mad will not put your name on a deed. Being mad will not build a portfolio. The folks you are mad at, are not losing sleep.

You have two choices. Stay mad and stay broke, or get educated and get positioned. No government program walking through that door to hand you the keys to wealth. You got to go get it. And step one is understanding what is actually happening, so you stop blaming yourself for a game you did not even know you was playing.

Coleman's Final Thought

The dollar in your pocket is not just money. It is a scoreboard, and the scoreboard keeps getting reset by people who never told you the rules. Quantitative easing and financial repression are not conspiracy theories. They are tools, and like any tool, they help whoever knows how to pick them up.

If you only know how to earn, save, and spend, you are playing checkers in a chess match. If you learn how to own, leverage, and compound, you start playing the same game the wealthy have been playing for generations. The information is out here now. The excuses are running out.

For anybody who learns better through video, this breakdown explains a lot of what I just walked you through.

https://www.youtube.com/watch?v=HVfCz0_G-Xs

Stay sharp. Stay positioned. Build something your grandkids inherit.

Topics: quantitative easing, financial repression, inflation, middle class wealth, real estate investing, index funds, VTSAX, ownership economy, generational wealth, financial literacy, asset allocation, dollar devaluation, retirement planning, economic education, wealth building, fixed rate mortgage strategy, central banking, monetary policy

Connect with CPRFIRM Website: https://cprfirm.com AI Tools: https://millionairex.ai Podcast: Diversified Game Podcast, available on all major platforms https://www.youtube.com/watch?v=OspAa1z9DYk